Retiring to Italy?

Italy’s 7% Flat Tax for Pensioners (2026 Update) – Complete Guide for UK Expats

Italy offers some of the most attractive tax regimes in Europe for new residents — but the rules differ depending on whether you are retiring, relocating for work, or moving as a high-net-worth individual. In 2026, Italy operates four distinct incentive regimes, including the well-known 7% pensioner tax and the €300,000 flat-tax option for wealthy new residents. Choosing the wrong structure can be costly, so understanding the differences is critical before triggering Italian tax residency

A five-step guide to one of Italy’s most attractive tax incentives for foreign retirees

If you’ve spent your working life in the UK diligently building your pension, you may already know the unfortunate reality: if you don’t spend it, a significant portion may ultimately return to HMRC.

But what if there were a way to enjoy more of your retirement income—somewhere warmer, slower-paced, and far more tax efficient?

2026 Update: Italy now has four distinct “new resident” tax regimes — and the wrong choice can be costly.

If you’re planning a move to Italy, it’s important to understand that the popular “7% flat tax” for retirees is only one of several incentives — and each applies to a different type of person (and in some cases, a different part of Italy).

Here are the four regimes most often relevant to UK families relocating in 2026:

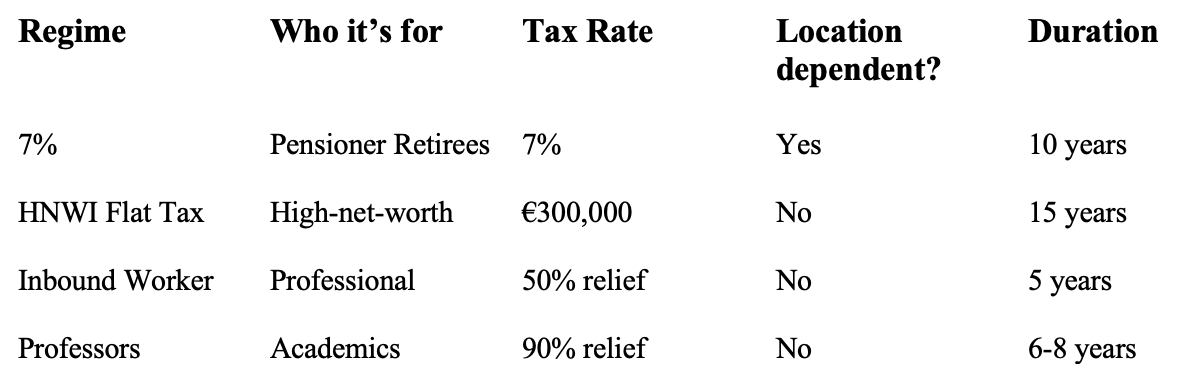

Retiree 7% regime (foreign pensioners) – a flat 7% substitute tax on eligible foreign-source income, typically available for up to 10 years, but only if you move to a qualifying municipality (location is critical).

HNWI “new residents” flat tax (non-dom style) – a fixed annual charge of €300,000 (from 1 Jan 2026) for foreign-source income, designed for high-net-worth individuals.

Inbound workers (“impatriate”) regime – generally 50% tax relief on employment/self-employment income (with a €600,000 cap on the eligible income), introduced from 2024, aimed at people relocating to work in Italy.

Professors & researchers – a specialist regime where 90% of qualifying income can be excluded from IRPEFfor eligible academic/research roles.

This guide focuses on the retiree 7% regime — but if you’re moving as a working professional, entrepreneur, or high-net-worth family, the optimal route can look very different.

Italy’s Regime per Pensionati Esteri—commonly referred to as the 7% Flat Tax Regime for Foreign Pensioners—offers just that. It allows eligible individuals to pay a flat 7% tax on foreign pension and overseas income for up to 10 years. No sliding scale, no stealth levies—just a clear, attractive rate.

So, how does it work? And what do you need to do to qualify?

Italy’s “HNWI flat tax” is more expensive from 2026

If you’ve heard that Italy offers a “non-dom” style option with a fixed annual payment on foreign income, that is a different regime to the 7% pensioner incentive.

From 1 January 2026, the annual substitute tax for the HNWI “new residents” regime increases to €300,000 per year, and the charge for each eligible family member is widely summarised as increasing to €50,000.

This regime can be highly effective in the right circumstances — but it is not designed for most retirees, and it’s one reason we always consider properly the move before you become Italian tax resident.

Step 1: Check Your Eligibility

This regime isn’t available to everyone, but if you're British with pension income and some flexibility on where you live, you may well qualify. Here’s what’s required:

You receive a foreign pension

This includes your UK State Pension, personal pensions, and occupational schemes.

(Note: Income from ISAs, onshore bonds, and Italian pensions does not qualify.)You haven’t recently lived in Italy

You must not have been an Italian tax resident in the five tax years prior to your move. Italy is welcoming new residents—but not returnees.You relocate to a qualifying municipality

The regime is available only in towns with fewer than 20,000 residents in southern regions such as Sicily, Calabria, Sardinia, Apulia, Basilicata, Campania, Molise, and Abruzzo, or in certain earthquake-affected municipalities in Umbria, Marche, and Lazio.

(Think: quiet hill towns, local markets, and Mediterranean charm.)You register correctly

You must obtain a Codice Fiscale (Italian tax code) and register as a resident (Anagrafe della Popolazione Residente) at your local town hall. Paperwork is essential—get this right from the outset.

Step 2: Establish Italian Tax Residency

To benefit from the regime, you must become tax resident in Italy by meeting all of the following criteria:

Spend at least 183 days per year in Italy

Move your centre of vital interests—such as your main home, personal ties, and daily life—to Italy

Be formally listed in the Anagrafe (resident population registry)

Step 3: Elect the 7% Regime

There is no standalone application form or certificate. You must simply elect the regime through your first Italian tax return.

Timing is critical. If you fail to elect the regime in that initial return, the opportunity is lost permanently.

Step 4: Understand the Duration and Limitations

The regime is available for 10 consecutive tax years—and it cannot be extended.

There are a few key limitations:

If you move to a non-qualifying municipality, you forfeit the benefit

If you revoke the regime, you cannot re-enter

If you fail to comply with the filing requirements, the regime is terminated

Like any favourable tax arrangement, it rewards careful planning and consistency.

Step 5: Know the Benefits—and What Still Applies

This is where the regime truly stands out:

Flat 7% tax on all qualifying foreign income, including pensions, overseas rental income, and investment returns

No Italian wealth tax (IVIE or IVAFE) on foreign assets or property

Italian-sourced income remains subject to ordinary income tax rates (IRPEF)

Inheritance and gift tax rules remain unchanged—cross-border estate planning remains essential

Planning to Relocate in 2026? You May Still Qualify

If you're still UK-resident but considering a move to Italy in the near future, it’s not too late.

Also worth noting: while the retiree 7% regime is location-dependent, the HNWI flat-tax option becomes materially more expensive from 2026 — so families considering Italy for lifestyle reasons and complex income streams should sanity-check which regime (if any) is realistic before they trigger residency.

Here's the optimal path if you're targeting a 2026 relocation:

Avoid triggering Italian tax residency in 2025

Move to a qualifying town during 2026

Register correctly and elect the 7% regime in your 2027 tax return, covering your 2026 income

In tax planning—just as in investing—timing matters.

Important Note

Italian tax incentives are highly technical, and eligibility often depends on facts on the ground (where you live, when you become resident, your income types, and how you file). Rules can also change between budget cycles. This article is general information — it is not personal tax or legal advice. Before acting, take specialist cross-border advice (UK + Italy). If helpful, MiraClair Wealth can coordinate the planning with an Italian tax professional so the chosen regime (and your timing) is defensible.

Quick sense-check: which regime is most likely relevant?

Retired with foreign pensions + flexible on location: start with the 7% regime (this guide).

Moving to Italy to work (employed or self-employed): explore the inbound workers (impatriate) regime.

Academic/research appointment in Italy: check the professors & researchers regime.

Very high foreign income / complex international structure: consider whether the €300,000 HNWI flat-tax is relevant (often alongside wider structuring).

With the right planning and professional guidance, you could enjoy la dolce vita.